When you need a loan, do you ever think, “My credit score…What’s that about?”

Well, during our next Money Chat, Mike Bonn is going to answer all of your questions. He’s also going to share insider tips on how to raise your score so you can get the best loan possible.

Want to join Mike’s Money Chat? Then register for FREEhere.

Mike will answer common questions like:

Is this based on my credit?

Will you pull my credit?

How can I boost my credit score?

What score do I need to get the best rates?

By the end of the Money Chat, you should have a much better grasp of how your credit score impacts your loan options…and, more importantly, your cash flow and profits.

Attention Real Estate Investors: Introducing The Cash Flow Mortgage Company!

At Investor Real Estate Loans, we decided it was time to change our name to convey who we REALLY are. That’s why we chose to call ourselves The Cash Flow Mortgage Company.

Our new business name represents exactly who we are and what we focus on: Cash flow!

As a mortgage company, we strive to provide real estate investors with the best loans possible, meaning we offer plenty of options and flexibility. Because every investor is different and needs a loan that fits THEIR needs (not ours).

We help all of our clients achieve cash flow success through 3 key strategies:

Lowering your finance costs. Because the lower costs, the more money you make.

Lowering the amount you have to put into the purchase of a rental property. We like to call this the 2-Step Process, but some know it as BRRRR or a $0 down rental purchase. Whatever the case, it’s the correct way to handle the loan side of your investments, and it’s very important if you want to boost your cash flow.

Use quick, proven strategies to raise your credit score. Why? Because the higher your credit score, the better your interest rates. And the better your interest rates, the more money you save every month. We like to call this your Return on Credit.

We strive to constantly focus on these 3 pillars of our business so that you have plenty of options to increase your cash flow. Because we’re eager to set you on a path that helps you make the kind of money you need to live the life you want.

Welcome to the new and improved Cash Flow Mortgage Company. We can’t wait to chat with you about your value-add plans!

https://thecashflowmortgagecompany.com/wp-content/uploads/2021/04/JENNAS-YouTube-Thumbnails-3-1.png7201280Jenna Weldonhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgJenna Weldon2021-04-06 09:40:462021-08-11 12:16:52Attention Real Estate Investors: Introducing The Cash Flow Mortgage Company

Real Estate Funding Solutions: Welcome to The Cash Flow Mortgage Company

If you’re looking for fast real estate funding from a team that truly cares about your cash flow, then welcome to the Cash Flow Mortgage Company.

Because we believe that cash flow makes life flow!

The Cash Flow Mortgage Company is a rare, one-stop-shop for all your real estate investment deals. Gone are the days of working with multiple lenders for one property. We have everything you need to generate positive cash flow and make life a whole lot easier.

Non-traditional and hard money loans are perfect for fix and flips, rentals, and BRRRRs, and other value-add properties. Furthermore, they’re ideal for real estate investors who need to move FAST or might need to get creative with qualifications. For example, if you don’t have tax returns (or don’t want to use them), then we have a loan for you. Or if you’re real estate portfolio needs some work, we can help you build it so you can eventually apply for a long-term bank loan.

Traditional funding

If you’ve got the qualifications, then we’ve got long-term, low-rate loans for you!

If you want to ensure your cash flow doesn’t take a major hit when the market is tight, or if you’re stuck in a project and need temporary funding, then a bridge loan is perfect.

The better your credit score, then the better your interest rates. And the better your interest rates, then better your loan products. Which means you spend way less money every month.

Ready to get going? Great, we’re here to help. Our team is eager to set you on a path the helps you make the kind of money you need to live the life you want!

https://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/JENNAS-YouTube-Thumbnails-1.png7201280Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2021-03-16 08:35:422021-08-11 12:33:52Real Estate Funding Solutions: Welcome to The Cash Flow Mortgage Company

Are you trying to close a real estate deal, but your funding was rejected? Are you wondering, “Why did my bank say no?”

Well, you’re not alone. Many real estate investors always been told: Find a bank and create a relationship with them. If you do, then life (and loans) will be easy.

So, why, after building these so-called relationships do banks still say no every time you apply for a real estate loan?

How many of us have been in this situation? Well, probably most of us.

But, why?

The reason most banks say no is because they only have 1-2 options for real estate investors. At best! And, wait for it, you probably don’t currently fit in their tiny, little boxes.

The truth is, banks carry very limited options for real estate investors.

Banks have many loans coming in their door. Too many. That means they can cherry pick. If it doesn’t fit in their itty-bitty box, they can just tell you, “No.”

So, you probably won’t fit in most banks’ small, strict, picky boxes if you:

Are a new investor.

Like to write everything off on your tax returns legally.

Want to refinance before you own a property for an entire year.

We’re talking about 97% of banks.

Even worse, banks won’t want to refer you to someone who can say yes. Because then you’d start asking too many questions on why they can’t give you a loan. Banks might not want your real estate investment loan, but they definitely want to keep your deposits and bank accounts.

The inside secret here is you need to call a lot of banks until you find one that’s still lending to investors and has a loan for you.

But be warned!

No bank will agree to close a real estate loan for you if your income doesn’t fit inside that tiny, little box of theirs.

You also always need tax returns with banks, and they need to be the type of tax returns where you can’t write everything off. And here’s the kicker of it all: You might find a bank that works for you, but then they decide to stop lending to investors. It just happened here in Colorado. One of the top investor banks just stopped lending.

So, when banks say no to you, understand that this is their usual response. You always have to remember they have limited products and limited amount of funds to lend out.

But don’t get discouraged!

Just look for a lender who focuses on real estate investors and offers options.

Because, really, there are HUNDREDS of options for investors. Options for:

https://thecashflowmortgagecompany.com/wp-content/uploads/2020/12/JENNAS-YouTube-Thumbnails-5.png7201280Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2020-12-11 08:52:252021-08-11 13:37:08Real Estate Deal: Why Did My Bank Say No?

Check out this cozy little hold-and-rent property our client purchased Greeley, Colorado! This deal was funded using a Hard Money Mike loan.

We love seeing our clients’ success stories and look forward to checking in on the progress with their investments.

Ready to fund your own investment property deal? Chances are good that we can help!

Hard Money Mike is a lender based in Colorado. We regularly lend money on all types of commercial-based properties. So whether you have your eye on a potential fix-and-flip, vacant land, whole tailing, or a builder bridge loans, we’re happy to help make your investment property dreams come true.

We even lend on deals in several states outside of Colorado, so don’t let our location stop you from achieving your investment goals. If we’re not yet lending in your state, we’re still happy to discuss your numbers and plans with you to make sure you’re on the right track.

In the market for a property in the single-family or commercial sector? Our sister company The Cash Flow Mortgage Company funds investor loans on those, too! We’ve got a lending solution to most investment opportunities, so let’s get you on the path to investment property greatness.

Questions or just need help deciphering your numbers? Feel free to reach out!

Hard Money Mike 303-539-3000

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

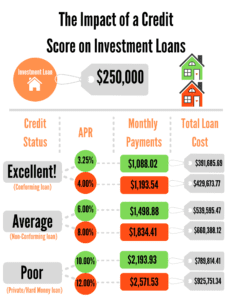

How much money might a lackluster credit score be costing you over the life of your investment business?

You probably hear a lot of talk in the mortgage industry about your credit score and the effect it can have on your interest rates, but do you really have an idea of how much it’s affecting your bottom dollar?

Do you know how to determine your Return on Credit (ROC)?

Can you crunch the numbers to figure out how much your score is helping your cash-flow (or how much money it’s sucking out every month?)

These calculations can get complicated, but the takeaway here is that a less-than-stellar score can really be costing your tens of thousands of dollars over the lifetime of your loan. And when your loan is on an investment property, (or several,) you may as well be lighting your profits on fire.

We want to help! Contact our team so we can help you see where you’re currently at, and where you could be going instead.

Let’s get you to your goals faster by trimming some of the fat from your financing!

Hard Money Mike is a lender based in Colorado offering services in several states. We lend money for all varieties of commercial-based properties. So whether you’re trying to finance a fix-and-flip, vacant land, whole-tailing, or looking for a builder bridge loan, we’ve got you covered.

Call Mike Bonn at: 303-539-3000 or email Mike@HardMoneyMike.com

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

https://thecashflowmortgagecompany.com/wp-content/uploads/2020/06/jp-valery-mQTTDA_kY_8-unsplash-scaled.jpg17072560Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2020-06-08 09:55:222020-06-11 10:55:59What’s the Cost of Your Credit Score?

For some of you, they do. For others, you might be left thinking, “But wait! What if I’m not going to keep the property for 24 or 30 years?At what point does it actually make sense to refinance?”

However, if you are not going to keep the property through the next 30 years, you’ll need to look hard at what the costs will be over the expected period. The key here is determining which path will cost you more money and which one will keep more in your pocket.

GOAL: Keep more money in your life and less in the hands of bankers.

Let’s look at an example:

You’re planning to keep a property for 3 years and then sell it. The question is, what will put more money in your pocket and cost you the least over those next 3 years?

Here is how we figure this out:

Step 1: Ask your mortgage company to run an amortization chart on your current loan and your new loan.

2: Then, pull your principal and interest from your current mortgage company’s website.

3: Next, ask your mortgage broker to give you the principal and interest from the new loan.

4: On each loan, multiply the payments by 36 (the 3-year window before you sell the property) and add the balance of your loan at the end of 3 years.

5. Lastly, compare notes and find out what would be the lowest amount. This is the one that will keep more money in your pocket.

Ultimately, this is just a pure and simple scenario of determining exactly how much the loan will take out of your pocket over the course of 3 years. We’re not looking at monthly cash flow, because true dollars out are pure and simple. This is your true cost out of your pocket.

If you need help, we’re happy to step in. Give us a call, and we can run all the numbers for you and see if it makes sense. If it does, we can help you out even further by securing low rates and costs on your refi!

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

https://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svg00Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2020-06-05 12:14:522020-06-11 10:56:33How to Know When a ReFi Makes Sense

Thankfully, it’s looking like another great week for standard conventional mortgage rates.

So far this week, all evidence is pointing towards increasing stability and improvements on the conventional mortgage front.

Depending on whether you pay your mortgage person points or you have them wrapped into your loan, rates fluctuate between low 3’s and low 4’s.

We’re seeing great rates on the conforming side.

Every week, the non-traditional loans are reappearing with increased frequency.

Some lenders have decreased credit score requirements to 680.

Rates are still on average above 7%, but signs are showing that they will drop soon.

LTVs are inching higher, but not to the degree we have seen them in the past.

In short: conventional mortgage interest rates are really good. But what does that mean for you?

How do you know when it’s smart to refinance your rental (or any) property?

Let’s face it: as rates drop, the question of whether or not to refinance runs through all our minds.

Would you like to find out (without the sales pitch from your mortgage person?)

Anyone can crunch the numbers in just a few minutes with just a few items.

Yes. It involves math. But we swear it’s EASY.

For now, all you need is a piece a paper, a pen, a calculator, and your mortgage information. (You can pull this info directly from your mortgage company’s website). Then, follow these three steps:

Step 1: Locate the amount you pay monthly for principal and interest. (Ignore everything but your principal and interest (i.e. taxes and insurance).

Step 2: Locate the number of months remaining on your loan.

Step 3: Multiply your monthly payment by the number of months you have left on your loan.

That’s it!

Let’s look at an example:

A: Your monthly principal and interest payment is $1,200.

B: You have 288 payments left on your loan.

C: $1,200.00 X 288 = $345,600

(Scary sometimes to see how much you really owe, isn’t it? Don’t panic.)

Now, let’s say that you have an opportunity to refinance and lower your interest rate with a new payment of $1,100. Should you do it?

Let’s take a look:

On your new loan, you’d pay $1,100.00 for 30 years (or 360 months). That’s $1,100.00 x 360 = $396,000.00

If you refinance, you’d increase your monthly cash flow $100.00. However, as a result, you’d pay an extra $50,400.00 over the life of your loan!

So, is the extra $100/month worth an extra 72 months (6 years) of mortgage payments? Does refinancing make sense for you financially? Well, that’s up to you.

Perhaps cash flow is more important at this time in your business life and paying the extra years is ok with you. That’s a decision only you can make. At least when you know all the numbers, you can make your call an educated one.

Try it on all your loans and find out what makes sense for you!

Your payments __________________ Months remaining _______________

Total remaining to be paid ___________________

Okay, we’re sure a few questions are swimming around in your head, so we’ll see if we can answer some of the most common ones upfront:

Q: “What if I’m not going to keep the property for 24 or 30 years? At what point does it make sense to refinance?”

A: That’s coming up in the next article.

Q: “What if I want to use those savings and pay down my mortgage?”

A: We’ll be addressing that in a future article as well.

Q: “What is my breakeven interest rate?”

A: There are so many paths you can go down and we’ll cover as many as we can. We’ll also provide a tool for you to run all these scenarios.

Today, it’s all about knowing your raw numbers.

Want an investor tool that can run these numbers (plus your breakeven rate and many more) in seconds? We have one in the works. Just get on our contact list, and we’ll let you know when it’s ready!

By knowing these numbers, you can save tens of thousands on each refinance.

Don’t feel like doing this or worry the math might overwhelm you? No worries! Shoot us an email with your current statement and we can run them for you.

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

Nobody does fix-and-flip curb appeal like these Dallas clients.

Check out these amazing Before-and-After photos of this Dallas Fix-and-Flip!

These clients did an amazing job transforming this living room into a much more liveable space.

From dark and cave-like, to light and inviting, this bedroom looks pretty dreamy to us!

From cluttered to cool, this kitchen got a pretty serious glow-up.

Not even the bathroom escaped noticed in this impeccable flip!

We’re still in awe of this amazing fix-and-flip investment deal from our Dallas area clients. A little imagination and some investment capital can go a long way towards transforming a haggard house into an updated future home!

We never tire of watching our clients change the face of their neighborhoods in a positive way. This property is a shining example of what the real estate investing community is all about: improving a neighborhood and enjoying a profitable rehab!

Looking for a hard money loan to fund your own flip? Look no further.

How do you take the guesswork out of getting your deals funded for rehab projects like this one? Simple: By partnering with Hard Money Mike.

Hard Money Mike is a lender based in Colorado. We offer a large pool of lenders so we can be sure to find the right fit for your project. We regularly lend money for all types of commercial-based properties. So whether your project is a fix-and-flip, land, whole-tailing, or a builder bridge loan, we have you covered.

If this flip has you feeling inspired, we want to know about it! Contact Mike Bonn at 303-539-3000 or email Mike@HardMoneyMike.com to start exploring your lending options!

Refinancing may have just become more expensive for both rate and lower LTVs.

Wow, what is this? The powers that be are still messing with our beautiful lending world. It’s not a shock that government officials seem more focused on getting votes at the cost of property owners and mortgage companies, encouraging tenants not to pay rents and not lending a hand with evictions.

What We Know:

Mortgage rates are so low right now (in the mid 2’s for owner-occupied, and low 3’s for investors) that still-employed buyers should be running out and buying homes left and right. After all, the number one reason buyers purchase is that they can fit the payment into their monthly budget. We should be seeing mortgage companies throwing money out to everyone. We should see buyers buying and investors refinancing (increasing that cashflow without adding more properties.)

So why isn’t that happening?

In short- our government is hard at work wreaking havoc in the lending markets, making it harder for all of us to get a loan, especially refinances.

Sure, it sounds good in theory: Allow anyone who wants to defer a payment or 4 during an economic crisis to do so, without proving any reason based on financial hardship.

How does this impact us all? Glad you asked.

If a lender helps someone out and refinances them and they decided to go directly into forbearance, (yes, people WERE doing cash-out refinances with the plan of deferring payments to take advantage of the government’s kindness,) that lender cannot sell or move that loan off of their books to those that service FHA, VA, Conventional loans, etc, unless they want to take pay a huge fee. So, they decide to hold the loans, thus filling up their lending bucket.

So what happens next? The lenders don’t want to take a chance that a percentage of people are going to take advantage of this opportunity, so they raise the cost of refinancing for everyone. On top of that, they will start lowering the LTVs (loan-to-value ratios,) making the box for traditional financing harder for all.

Yes, obviously those that need mortgage forbearance should be able to use it, but it’s the ones who are not in financial need that are making these numbers grow, creating more costly financing for us all.

Key findings of MBA’s Forbearance and Call Volume Survey – April 13-19, 2020

Total loans in forbearance grew relative to the previous week (from 5.95% to 6.99%.) In comparison, only 0.25% of all loans were in forbearance for the week of March 2.

By investor type, Ginnie Mae loans grew the most relative to the prior week: from 8.26% to 9.73%.

The share of Fannie Mae and Freddie Mac loans in forbearance increased relative to the prior week: from 4.64% to 5.46%.

The share of other loans (e.g. private-label securities and portfolio loans) in forbearance increased relative to the prior week: from 6.43% to 7.52%.

Forbearance requests as a percent of servicing portfolio volume (#) dropped relative to the prior week: from 1.79% to 1.14%.

What You Can Do:

Keep up with your payments if you’re able. The more of us that are paying on time and in full, the quicker the lenders will start to relax and start loaning again. Everyone wins.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.